This content is owned or licensed by Cboe Global Markets, Inc. or its affiliates (“Cboe”) and protected by copyright under U.S.

and international copyright laws. Other than for internal business purposes, you may not copy, reproduce, distribute, publish,

display, perform, modify, create derivative works, transmit, or in any way exploit the content, sell or offer it for sale, use the

content to construct any kind of database, or alter or remove any copyright or other notice from copies of the content.

Cboe Options Exchanges

Binary Order Entry

Specification

Version 2.11.67

August 28, 2024

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 2

Contents

1 Introduction .............................................................................................................................................. 6

1.1 Overview ...................................................................................................................................................... 6

1.2 Certification Requirement ............................................................................................................................ 6

1.3 Document Format ........................................................................................................................................ 6

1.4 Hours of Operation ...................................................................................................................................... 6

1.4.1 Holiday Sessions (C1 only) ........................................................................................................................ 7

1.5 Data Types .................................................................................................................................................... 7

1.6 Optional Fields and Bit fields ........................................................................................................................ 8

1.7 Protocol Features ......................................................................................................................................... 9

1.7.1 Architecture and Message in Flight Settings ............................................................................................ 9

1.7.2 Complex Instruments and Signed Prices (C1, C2, and EDGX only) ........................................................... 9

1.7.3 Done For Day Restatements .................................................................................................................... 9

1.7.4 Carried Order Restatements .................................................................................................................. 10

1.7.5 Cancellation of Carried Orders Between Trading Sessions .................................................................... 10

1.7.6 Display Indicator Features ...................................................................................................................... 11

1.7.7 Default Exchange Risk Protections ......................................................................................................... 11

1.7.8 Risk Root ................................................................................................................................................. 15

1.7.9 Market Maker Trade Notifications (C1 Only) ......................................................................................... 15

1.7.10 Cabinet and Sub-Cabinet Orders (C1 Only) ............................................................................................ 15

1.7.11 Auction Orders ....................................................................................................................................... 15

1.7.12 Port Types .............................................................................................................................................. 15

1.7.13 Floor Routing (C1 Only) .......................................................................................................................... 17

1.7.14 Stale NBBO ............................................................................................................................................. 19

2 Session ..................................................................................................................................................... 20

2.1 Message Headers ....................................................................................................................................... 20

2.2 Login, Replay and Sequencing .................................................................................................................... 20

2.3 Sequence Reset .......................................................................................................................................... 21

2.4 Heartbeats .................................................................................................................................................. 21

2.5 Logging Out ................................................................................................................................................ 21

3 Session Messages ..................................................................................................................................... 22

3.1 Member to Cboe ........................................................................................................................................ 22

3.1.1 Login Request ......................................................................................................................................... 22

3.1.2 Logout Request ...................................................................................................................................... 25

3.1.3 Client Heartbeat ..................................................................................................................................... 25

3.2 Cboe to Member ........................................................................................................................................ 26

3.2.1 Login Response....................................................................................................................................... 26

3.2.2 Logout .................................................................................................................................................... 28

3.2.3 Server Heartbeat .................................................................................................................................... 29

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 3

3.2.4 Replay Complete .................................................................................................................................... 30

4 Application Messages ............................................................................................................................... 31

4.1 Member to Cboe ........................................................................................................................................ 31

4.1.1 New Order .............................................................................................................................................. 31

4.1.2 New Order Cross (C1 and EDGX Only) .................................................................................................... 32

4.1.3 New Complex Order (C1, EDGX, and C2 Only) ....................................................................................... 36

4.1.4 New Order Cross Multileg (C1 and EDGX Only) ..................................................................................... 38

4.1.5 Cancel Order .......................................................................................................................................... 42

4.1.6 Modify Order .......................................................................................................................................... 44

4.1.7 Quote Update ......................................................................................................................................... 46

4.1.8 Quote Update (Short) ............................................................................................................................. 49

4.1.9 Purge Orders .......................................................................................................................................... 51

4.1.10 Reset Risk ............................................................................................................................................... 53

4.1.11 New Complex Instrument (C1, C2, and EDGX Only) ............................................................................... 55

4.1.12 Add Floor Trade (C1 Only) ...................................................................................................................... 57

4.1.13 Floor Trade Confirmation (C1 Only) ....................................................................................................... 60

4.1.14 Delete Floor Trade (C1 Only) .................................................................................................................. 62

4.2 Cboe to Member ........................................................................................................................................ 64

4.2.1 Order Acknowledgment ......................................................................................................................... 64

4.2.2 Cross Order Acknowledgment (C1 and EDGX Only) ............................................................................... 65

4.2.3 Quote Update Acknowledgment ........................................................................................................... 67

4.2.4 Order Rejected ....................................................................................................................................... 69

4.2.5 Cross Order Rejected (C1 and EDGX Only) ............................................................................................. 71

4.2.6 Quote Update Rejected .......................................................................................................................... 72

4.2.7 Order Modified ...................................................................................................................................... 73

4.2.8 Order Restated ....................................................................................................................................... 74

4.2.9 Quote Restated ...................................................................................................................................... 76

4.2.10 User Modify Rejected ............................................................................................................................. 77

4.2.11 Order Cancelled...................................................................................................................................... 78

4.2.12 Quote Cancelled ..................................................................................................................................... 79

4.2.13 Cross Order Cancelled (C1 and EDGX Only) ........................................................................................... 80

4.2.14 Cancel Rejected ...................................................................................................................................... 82

4.2.15 Order Execution ..................................................................................................................................... 83

4.2.16 Quote Execution ..................................................................................................................................... 86

4.2.17 Trade Cancel or Correct ......................................................................................................................... 87

4.2.18 Purge Rejected ....................................................................................................................................... 89

4.2.19 Reset Risk Acknowledgment .................................................................................................................. 90

4.2.20 Mass Cancel Acknowledgment .............................................................................................................. 91

4.2.21 Purge Notification .................................................................................................................................. 92

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 4

4.2.22 Complex Instrument Accepted (C1, C2, and EDGX Only) ....................................................................... 94

4.2.23 Complex Instrument Rejected (C1, C2, and EDGX Only) ........................................................................ 97

4.2.24 Floor Trade Notification (C1 Only) ......................................................................................................... 98

4.2.25 Add Floor Trade Rejected (C1 Only) ..................................................................................................... 100

4.2.26 Floor Trade Confirmation Rejected (C1 Only) ...................................................................................... 102

4.2.27 Delete Floor Trade Rejected (C1 Only) ................................................................................................. 103

4.2.28 Delete Floor Trade Acknowledgement (C1 Only) ................................................................................. 105

5 Input Bitfields Per Message ..................................................................................................................... 106

5.1 New Order ................................................................................................................................................ 107

5.2 New Order Cross (C1 and EDGX Only) ...................................................................................................... 108

5.3 New Complex Order (C1, C2, and EDGX Only) ......................................................................................... 108

5.4 New Order Cross Multileg (C1 and EDGX Only) ....................................................................................... 109

5.5 Cancel Order ............................................................................................................................................ 109

5.6 Modify Order ............................................................................................................................................ 110

5.7 Purge Orders ............................................................................................................................................ 110

5.8 New Complex Instrument (C1, C2, and EDGX Only) ................................................................................. 111

6 Return Bitfields Per Message .................................................................................................................. 112

6.1 Order Acknowledgment ........................................................................................................................... 113

6.2 Cross Order Acknowledgment (C1 and EDGX only) ................................................................................. 115

6.3 Order Rejected ......................................................................................................................................... 117

6.4 Cross Order Rejected (C1 and EDGX Only) ............................................................................................... 119

6.5 Order Modified ........................................................................................................................................ 121

6.6 Order Restated ......................................................................................................................................... 123

6.7 User Modify Rejected ............................................................................................................................... 125

6.8 Order Cancelled ....................................................................................................................................... 127

6.9 Cross Order Cancelled (C1 and EDGX Only) ............................................................................................. 129

6.10 Cancel Rejected ........................................................................................................................................ 131

6.11 Order Execution ....................................................................................................................................... 133

6.12 Trade Cancel or Correct ........................................................................................................................... 135

6.13 Purge Rejected ......................................................................................................................................... 137

6.14 Purge Notification .................................................................................................................................... 139

6.15 Complex Instrument Accepted (C1, C2 and EDGX Only) .......................................................................... 141

6.16 Complex Instrument Rejected (C1, C2, and EDGX Only ) ......................................................................... 143

7 List of Optional Fields.............................................................................................................................. 145

8 Reason Codes ......................................................................................................................................... 165

8.1 Order Reason Codes ................................................................................................................................. 165

8.2 Quote Reason Codes ................................................................................................................................ 166

8.3 Order and Quote Subreason Codes ......................................................................................................... 167

9 List of Message Types ............................................................................................................................. 168

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 5

9.1 Member to Cboe ...................................................................................................................................... 168

9.2 Cboe to Member ...................................................................................................................................... 168

10 Port Attributes ........................................................................................................................................ 170

11 Support .................................................................................................................................................. 175

Revision History .............................................................................................................................................. 176

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 6

1 Introduction

1.1 Overview

This document describes Binary Order Entry (BOE), the Cboe proprietary order entry protocol.

Where applicable, the terminology (e.g., time in force) used in this document is similar to that used by the FIX

protocol to allow those familiar with FIX to more easily understand BOE. This document assumes the reader has

basic knowledge of the FIX protocol.

BOE fulfills the following requirements:

• CPU and memory efficiency. Message encoding, decoding, and parsing are simpler to code and can be

optimized to use less CPU and memory at runtime.

• Application level simplicity. State transitions are simple and unambiguous. They are easy to apply to a

Member’s representation of an order.

• Session level simplicity. The session level protocol (login, sequencing, replay of missed messages, logout)

is simple to understand.

While Cboe has strived to preserve feature parity between FIX and BOE where possible, some features may only be

available in one protocol or the other.

All binary values are in little Endian (used by Intel x86 processors), and not network byte order.

Each message is identified by a unique message type. Not all message types are used in all Cboe’s trading

environments globally. A listing of the supported message types is provided in Section 10 - List of Message Types.

All communication is via standard TCP/IP.

1.2 Certification Requirement

All customers must complete a formal certification in the appropriate Cboe Certification test environment before

production orders or quotes will be accepted by Cboe. Formal certification scripts can be found in the Cboe Customer

Web Portal. Customers may complete the formal certification using the Certification Tool app and selecting the

applicable certification script. Customers are advised to test all functionality they plan to use in production in the

Cboe Certification test environment.

1.3 Document Format

Blue highlighted sections highlight key differences between the Cboe US Options Exchanges (BZX Options Exchange

“BZX only”, Cboe Options Exchange “C1 only”, C2 Options Exchange “C2 only”, and EDGX Options Exchange “EDGX

only”).

1.4 Hours of Operation

All times noted are Eastern time zone (ET) based.

See the respective exchange websites for holiday schedules.

Cboe Options Exchanges support a Pre-Market Queuing Session that allows orders to be entered and queued prior

to the start of the Global Trading Hours (GTH) session and the Regular Trading Hours (RTH) session. The GTH Queuing

session allows SPX, VIX, and XSP orders marked as both GTH and RTH only order to be entered and queued. C1 also

supports a Curb session in addition to GTH and RTH sessions.

For more information on the Cboe Opening Process, please refer to the Cboe Opening Process Specification.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 7

Cboe Options Exchanges do not support a closing auction, but do support extended trading for options on select ETF

and index products. All orders remaining after the Regular Trading Session that are not eligible for Extended Trading

will be cancelled automatically. All orders remaining after the Extended session will be cancelled automatically.

Members will receive Order Cancelled messages for all automatically cancelled orders.

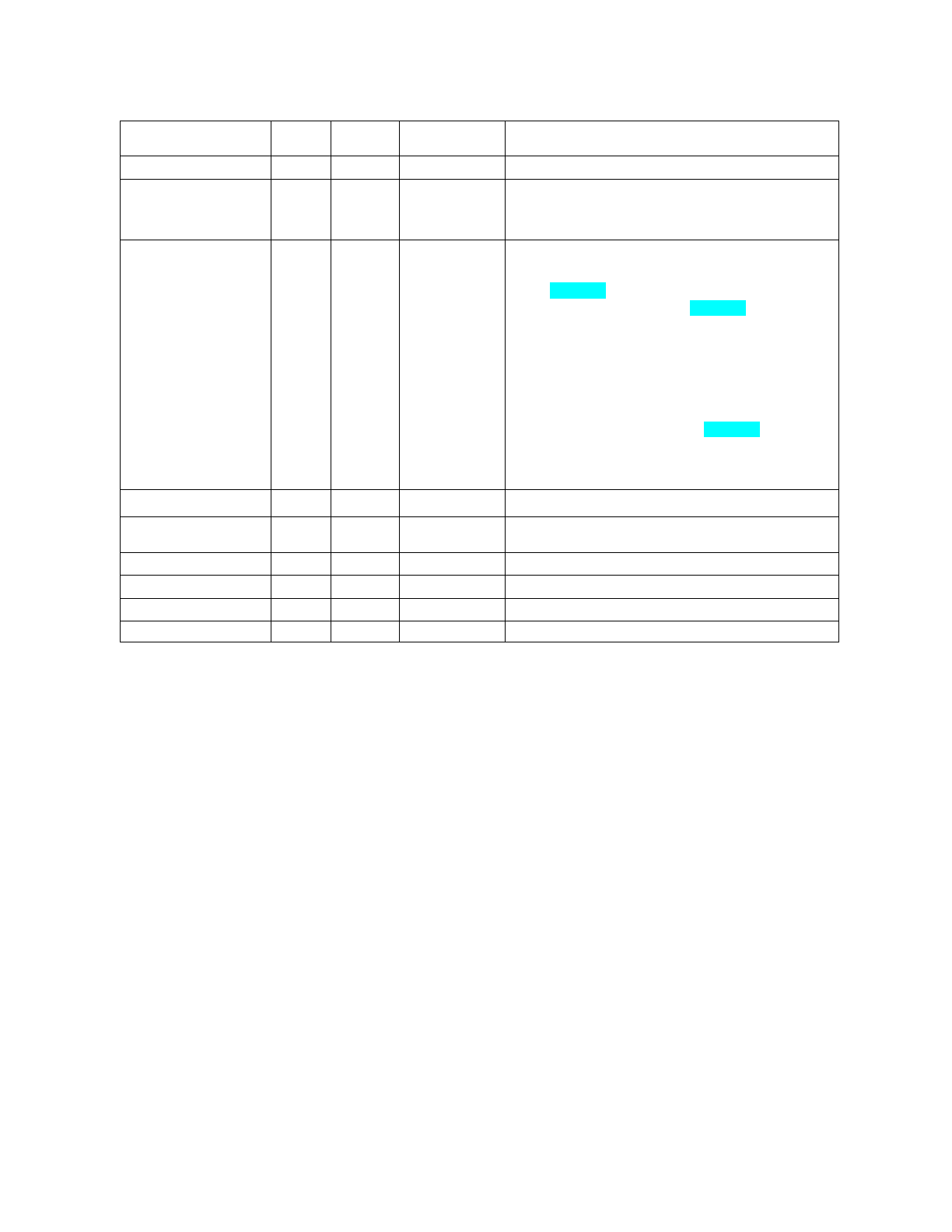

C1

C2

BZX

EDGX

Order

Acceptance

8:00 pm – 8:15 pm ET

(SPX/VIX/XSP)

7:30 am - 9:30 am

ET

(All Products)

7:30 am - 9:30 am

ET

(All Products)

7:30 am - 9:30 am

ET

(All Products)

7:30 am - 9:30 am ET

(All Products)

GTH

8:15 pm - 9:25 am ET (SPX/VIX/XSP)

N/A

N/A

N/A

RTH

9:30 am - 4:00 pm ET

(All Products)

9:30 am - 4:00 pm

ET

(All Products)

9:30 am - 4:00 pm

ET

(All Products)

9:30 am - 4:00 pm

ET

(All Products)

9:30 am - 4:15 pm ET

(Select ETF's/ETN's and Index

Products)

9:30 am - 4:15 pm

ET

9:30 am - 4:15 pm

ET

9:30 am - 4:15 pm

ET

Curb

4:30 pm – 5:00 pm ET

(SPX/VIX/XSP)

N/A

N/A

N/A

1.4.1 Holiday Sessions (C1 only)

On certain US-centric holidays, where European and/or Asian markets are open, trading is suspended for RTH and

Curb but continues for GTH, resulting in two sets of non-contiguous GTH sessions before RTH.

Figure 1: US Holiday Trading Hours

On days where the market closes early, RTH will conclude at 1:15 p.m. ET and there will not be a subsequent Curb

session. The market will remain closed until the next GTH session.

On certain International Holidays (i.e. New Years’ Day) there is no GTH or RTH trading and the C1 Options market is

closed. Notice will be sent prior to any holiday communicating the specific hours and sessions that will be available.

1.5 Data Types

The following data types are used by BOE. The size of some data types varies by message. All data types have default

values of binary zero, in both Member to Cboe and Cboe to Member contexts.

• Binary: Little Endian byte order, unsigned binary value. The number of bytes used depends on the context.

— One byte: FE = 254

— Four bytes: 64 00 00 00 = 100

• Signed Binary: Little Endian byte order, signed two's complement, binary value. The number of bytes used

depends on the context.

— One byte: DF = -33

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 8

— Four bytes: 64 00 00 00 = +100

• Binary Price: Little Endian byte order value, signed two's complement, eight bytes in size, with four implied

decimal places. So, if the value is -123,400, the actual value taking into account implied decimal places is

-12.34.

— 08 E2 01 00 00 00 00 00 = 123,400/10,000 = 12.34

— F8 1D FE FF FF FF FF FF = -123,400/10,000 = -12.34

• Short Binary Price: Little Endian byte order value, signed two's complement, four bytes in size, with four

implied decimal places. So, if the value is 12,300, the actual value taking into account implied decimal places

is 1.23.

— 0C 30 00 00 = 12,300/10,000 = 1.23

• Signed Binary Fee: Little Endian byte order value, signed two's complement, eight bytes in size, with five

implied decimal places. So, the value is -123,000 is -1.23 after taking account for the five implied decimal

places.

— 88 1F FE FF FF FF FF FF = 123,000/100,000 = -1.23

• Alpha: Uppercase letters (A-Z) and lowercase letters (a-z) only. ASCII NUL (0x00) filled on the right, if

necessary. The number of bytes used depends on the context.

• Alphanumeric: Uppercase letters (A-Z), lowercase letters (a-z) and numbers (0-9) only. ASCII NUL (0x00)

filled on the right, if necessary.

• Text: Printable ASCII characters only. ASCII NUL (0x00) filled on the right, if necessary.

• DateTime: Little Endian byte order, eight bytes. The date and time, in UTC, represented as nanoseconds

past the UNIX epoch (00:00:00 UTC on 1 January 1970). The nanoseconds portion is currently ignored and

treated as 0 (i.e. the times are only accurate to microseconds) on input, and will always be set to 0 by Cboe

in outgoing messages. However, Cboe may begin populating the nanoseconds portion at any time without

warning.

For example: 1,294,909,373,757,324,000 = 2011-01-13 09:02:53.757324 UTC.

• Date: Little Endian byte order, unsigned binary value, 4 bytes in size. The YYYYMMDD expressed as an

integer.

1.6 Optional Fields and Bit fields

Some messages such as New Order message and Modify Order message have a number of optional fields. A

count and number of bitfields in the message specify which optional fields will be present at the end of the message.

If a bit is set, the field will be present. Fields are appended to the end of the message. There is no implicit framing

between the optional fields. In order to decode the optional fields, they must be appended in a particular order to

the end of the message. The fields of the first bitfield are appended first, lowest order bit first. Next, the fields of the

next bitfield are appended, lowest order bit first. This continues for all bitfields. While certain reserved bits within a

defined bitfield are used within another Cboe market and will be ignored, bits that are reserved for future expansion

must be set to 0 when noted in the bitfield description.

The size, data type, and values for each field are described in Section 7 – List of Optional Fields.

Note that the set of optional fields returned for each Cboe to Member message type is determined at session login

(using the Login Request message); hence, the exact size and layout of each message received by the client

application can be known in advance. Any requested optional field, which is irrelevant in a particular context, will

still be present in the returned message, but with all bytes set to binary zero (0x00).

Each return message from Cboe to Member indicates the optional fields which are present, even though the Member

indicated during login which optional fields are to be sent. The reason for the inclusion (and duplication) is so that

each message can be interpreted on its own, without having to find the corresponding login request or response to

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 9

know which optional fields are present. So, for example, in a log file, decoding a message requires only that single

message.

Example messages are shown with each message type, which should help to make this concept clear.

1.7 Protocol Features

The exchange does not guarantee messages sent by Members/TPHs to the exchange, including through protocols

such as TCP. Members/TPHs are responsible to monitor the status of the messages they send to the exchange.

1.7.1 Architecture and Message in Flight Settings

Each BOE order handler process will allow a single TCP connection from a member. Connection attempts from

unknown source IP ranges will be blocked to prevent unauthorized access to BOE ports. The Cboe NOC should be

contacted in the event that a Member desires to connect from a new source IP range.

Each BOE order handler will connect, using a proprietary UDP protocol, to all matching units. Connections from order

handlers to matching engines are latency equalized. The connections between order handlers and matching units

are governed by an internal flow control mechanism to control burst rates.

The number of messages in flight between an order handler and a matching engine is 128. In addition, when the

total number of unacknowledged messages exceeds 1,024, the BOE order handler will stop reading from the

member-facing TCP socket. This will cause the order handler to stop removing bytes from the TCP receive buffer,

and will prevent the member from sending more TCP data once the member’s send buffer is full.

When the total number of unacknowledged messages falls below 960, the reading of the member facing TCP

socket will be resumed.

For message in flight counting purposes the following logic will be used:

• A new order message will count as one message;

• A new complex order with up to 100 legs will count as one message;

• A new order cross or new complex order cross auction message with one agency side and up to 10 contra

parties will count as one message;

• A quote update with up to 20 individual quote sides will count as one message.

• In contrast, a single TCP segment sent by a member containing two quote update messages, each with

five quote sides, will count as two messages

Cboe may either update the message in flight or the total number of unacknowledged messages settings with

notice. Changes to reduce either limit will be made only with two weeks’ notice. Cboe reserves the ability to

increase either limit immediately with notice.

1.7.2 Complex Instruments and Signed Prices (C1, C2, and EDGX only)

All price fields in the BOE protocol are signed values capable of accommodating complex instruments that can be

negative (See Data Types) for a description and an example of using the Binary Price type with a negative price). For

an example of the use of the Binary Price type with negative price values in an application message, see the example

BOE message in New Complex Order message.

1.7.3 Done For Day Restatements

Good ‘Til Cancel (GTC) and Good ‘Til Day (GTD) orders can result in order persisting between sessions. The Cboe

BOE protocol provides a mechanism for clients to request end-of-day restatement of GTC/GTD orders that will be

persisted to the next trading session. See Section Section 10 – Port Attributes for information on available port

attributes, including Done For Day Restatements.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 10

When enabled, Done For Day Restatement messages are sent to connected clients after the trading session ends,

for each order that will persist to the next trading session. Any time prior to the cutoff, customers may send Cancel

Order messages for any open GTC and GTD orders.

Done For Day Restatements are represented using Order Acknowledgement messages with the following optional

attributes set:

• BaseLiquidityIndicator = A (Added Liquidity), bitfield 5, bit position 7

• SubLiquidityIndicator = D (Done For Day), bitfield 7, bit position 1

To receive Done For Day Restatements, the Done For Day Restatement port attribute must be set (contact Cboe

Trade Desk), and customers must register to receive BaseLiquidityIndicator and SubLiquidityIndicator optional fields

on Order Acknowledgement messages via the Logon Request message (See Section 3.1.1 – Login Request for

details on registering to receive optional fields on a per-message basis). If the Done For Day Restatement port

attribute is set and the bitfield Logon Message registration for the Order Acknowledgement message does not

include but BaseLiquidityIndicator and SubLiquidityIndicator, the logon attempt will fail.

1.7.4 Carried Order Restatements

Good ‘Til Cancel (GTC) and Good ‘Til Day (GTD) orders can result in orders persisting between sessions. The Cboe

BOE protocol provides a mechanism for clients to request restatement of orders that have been carried forward

from the previous business day trading session. See Section 10 – Port Attributes for information on available port

attributes, including Carried Order Restatements.

When enabled, Carried Order Restatements are sent to connected clients for each product on the Options Exchange

for which orders have been carried forward from the previous business day trading session. Carried Order

Restatements are sent after connection establishment and before regular trading activity messages on a per-product

basis.

Carried Order Restatements are represented using Order Acknowledgement messages with the following optional

attributes set:

• BaseLiquidityIndicator = A (Added Liquidity), bitfield 5, bit position 7

• SubLiquidityIndicator = C (Carried), bitfield 7, bit position 1

To receive Carried Order Restatements, the Carried Order Restatement port attribute must be set (contact CFE

Trade Desk), and customers must register to receive BaseLiquidityIndicator and SubLiquidityIndicator optional fields

on Order Acknowledgement messages via the Logon Request message (See Section 3.1.1 – Login Request for

details on registering to receive optional fields on a per-message basis). If the Carried Order Restatement port

attribute is set and the bitfield Logon Message registration for the Order Acknowledgement message does not

include but BaseLiquidityIndicator and SubLiquidityIndicator, the logon attempt will fail.

1.7.5 Cancellation of Carried Orders Between Trading Sessions

GTC and GTD orders persist within the Cboe Options Exchanges between business days. On BZX, EDGX, and C2 the

latest time when GTC/GTD orders may be cancelled is 4:45 p.m. ET.

On C1 Options the latest time when GTC/GTD orders may be cancelled is 5:15 p.m. ET (15 minutes following the

close of the Curb Session).

GTC, GTD, and Day orders also persist between multiple GTH trading sessions on the same business day in connection

with a holiday. On US holidays, Cancel Order messages for GTC orders may be issued until 11:45 a.m. ET, which

is 15 minutes after the first GTH session ends at 11:30 a.m. ET. The Multi-Segment Holiday Day Order Handling port

attribute will enable Members to designate if Day orders are cancelled or preserved across holiday trading segments

comprising a single business date. See Section 10 – Port Attributes for information on available port attributes.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 11

1.7.6 Display Indicator Features

Orders are eligible for all of the sliding features described below. Quotes are eligible for the sliding behaviors

described below if they are received with a price that locks the NBBO and with a PostingInstruction eligible for price

sliding. Quotes that also cross the NBBO or displayed Cboe book will be accepted if within a configurable buffer

range through the NBBO or displayed Cboe book. The buffer is set to 5% with a minimum of $0.05 and a maximum

of $1.00.

For BZX only, quotes and orders that are marked as “Post Only” will execute against resting liquidity as a remover

and be charged applicable removal fee codes if the amount of price improvement of the removal execution exceeds

the expected rebate that the order or quote would have received if it had posted at its limit price.

Display-Price Sliding (BZX Only)

If the original limit price of the unexecuted remainder of a day order does not lock or cross the NBBO then Cboe

works the order at the original limit price while displayed at the nearest permissible quoting increment. If the

original limit price does lock or cross the NBBO then Cboe makes available Display-Price Sliding.

Display-Price Sliding adjusts the original limit price on entry to the locking price of the NBBO. It will be ranked and

worked at a price locking the NBBO but will temporarily adjust the displayed price to the nearest permissible quoting

increment. When the NBBO widens, the display price will be readjusted to the adjusted limit price. The display price

may be temporarily less aggressive than the adjusted limit price or working price.

Multiple Display-Price Sliding does not permanently adjust the original limit price on entry, but allows for Display-

Price slid orders to continue to have their display and working prices adjusted towards their original limit price based

on changes to the prevailing NBBO.

Contra-side Post Only orders that are received when a Display-Price Slid order is working at a locking price with the

NBBO will not result in a reject of a contra-side Post Only order but will instead result in the working price of the

Display-Price Slid order to be repriced to one penny away from the locking price.

Price Adjust (BZX, C1, C2, and EDGX Only)

If the limit price of an order does not lock or cross the NBBO, then the order will be ranked and displayed at the

nearest permissible quoting increment.

If the limit price of a Price Adjust eligible order locks or crosses the NBBO, the limit price will be adjusted on entry to

the locking price of the NBBO, while the displayed price and ranked price will be temporarily adjusted to the nearest

permissible quoting increment. Price Adjust orders will never be ranked at the locking price or at a non-displayable

price increment. If the NBBO widens, the displayed price and ranked price will be readjusted to the adjusted limit

price.

The limit price of a Multiple Price Adjust order will not be permanently adjusted on entry if the limit price crosses

the NBBO. The displayed price and ranked price will be the nearest permissible quoting increment and will be

adjusted towards the original limit price based on changes in the prevailing NBBO.

NoRescrapeAtLimit (BZX Only)

Applicable only to fully routable IOC orders (9303=R and 59=3). After walking the price down to the limit, there will

be no final scrape at Cboe and the cancel code will state “X: Expired” rather than “N: No Liquidity”.

1.7.7 Default Exchange Risk Protections

1.7.7.1 Market Order NBBO Width Protection for Simple Orders

Market Orders are rejected if the NBBO width is greater than 100% of the midpoint (with a minimum value of $5.00

and maximum value of $10.00).

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 12

Example

• NBBO = $1.00 x $4.00

• Midpoint =$2.50 x 100% = $2.50 (min of 5.00 is used instead)

• NBBO Width= $4.00 – $1.00 = $3.00

Even though the width is greater than 100% of the midpoint, Market Orders entered are accepted since the $5.00

minimum applies in this example.

1.7.7.2 Drill-Through Protection for Simple Limit Orders

Each simple limit order will be assigned a drill-through price that allows simple orders to be executed up to a

maximum capped price through the contra side NBBO at time of order entry. The drill-through mechanism will

repeatedly post the order at a more aggressive price. If the order reaches its limit price at any time during the

iterative drill-through process, the order will remain at its limit price and the drill-through protection mechanism will

not continue. The preset duration is one second.

Adjustments that would lock or invert an away displayed market will initiate a SUM auction. Eligible complex orders

may also initiate a COA throughout the iterative process.

Market orders submitted with a TimeInForce (FIX Tag 59) of Day along with elected stop orders will be eligible for

iterative drill-through price protection.

• Sell market orders will drill-through down to the minimum tick for the class where they will rest until

cancelled or executed in full.

• Buy market orders will drill-through to the maximum allowable price for the class where they will rest until

cancelled or executed in full.

• Market orders submitted with a TimeInForce of IOC will trade on arrival, capped at the first drill-through

price level.

Separate stop and stop limit orders elected as a result of the same election trigger (NBBO update or last sale) will all

use the same drill-through reference price. This may include orders with multiple stop prices if the election trigger

covers multiple price levels. When multiple stop orders are elected as a result of the same election trigger, they are

sequenced in time priority based on their order entry time.

• If an iterative drill-through protection is in progress, newly-elected stop and stop limit orders will join the

current drill-through price. The newly-elected stop and stop limit orders will be prioritized behind orders

already in drill-through.

• If no iterative drill-through is in progress, the initial drill-through reference price for stop and stop limit

orders elected by the same market data event will be set to the contra side NBBO

Triggered Market-On-Close and Limit-On-Close orders are handled the same as elected stop and stop limit orders

with respect to drill-through reference price and priority.

• Existing market-width checks prevent market orders from executing if the bid/ask width is wider than a

specified amount. This protection will be bypassed for triggered Market-On-Close orders and triggered stop

orders.

• Existing Fat Finger limit price reasonability checks reject limit orders priced at an overly-aggressive level.

Such protections will be bypassed for triggered Limit-On-Close orders and triggered stop limit orders.

The Drill-Through Price is calculated by taking the NBB or NBO and subtracting or adding, respectively, the Drill-

Through Amount from the table below. Calculated drill-through prices at an invalid pick increment for the class will

be widened to the next valid tick.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 13

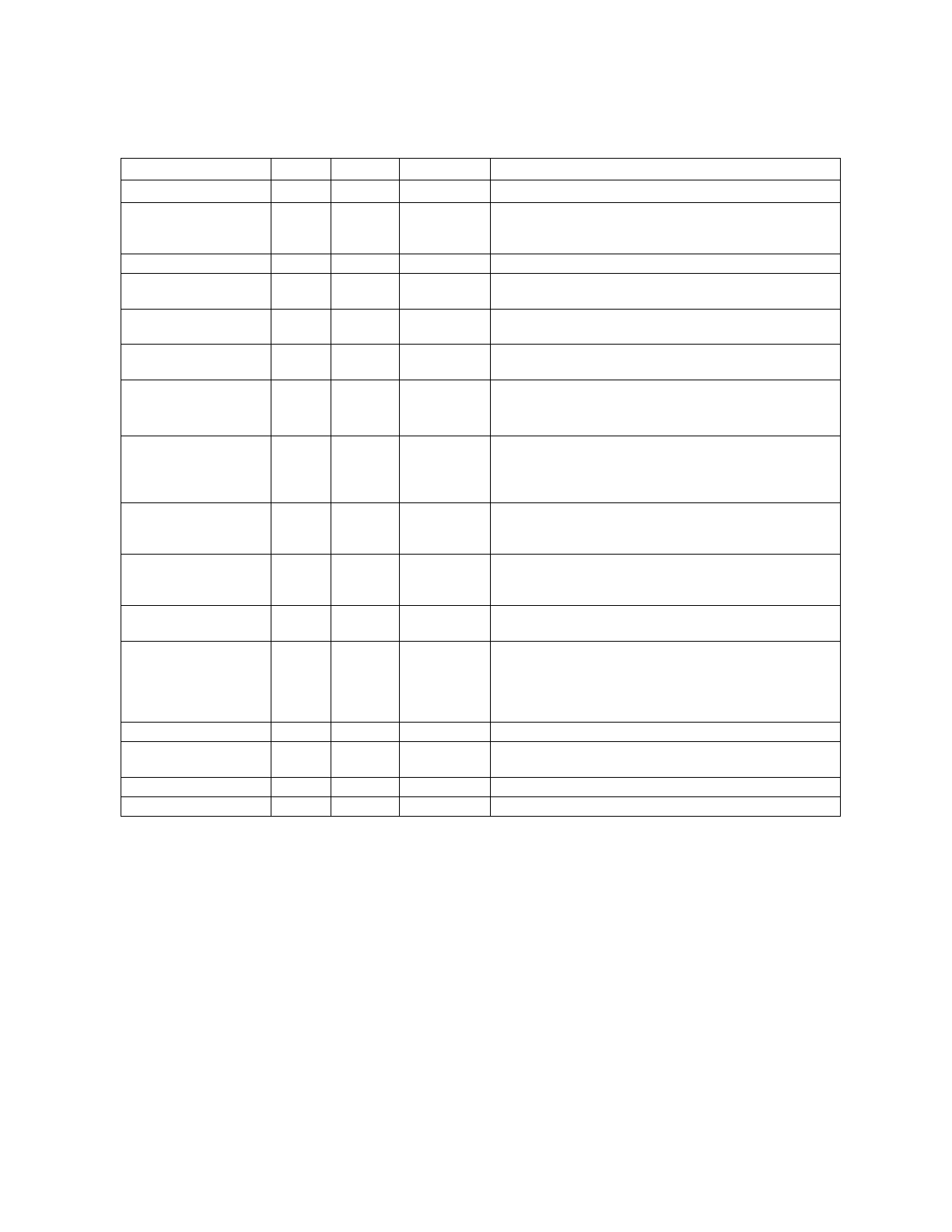

NBBO Price

Drill-Through Amount

(All Symbols)

$0.00 – $5.00

$0.10

$5.01 – $20.00

$0.20

$20.01 – $50.00

$0.30

$50.01 – $100.00

$0.40

$100.01 & Above

$0.50

Effective 09/16/24:

NBBO Price

Drill-Through Amount

(All Symbols)

$0.00 – $5.00

$0.05

$5.01 & Above

$0.10

1.7.7.3 Market/Limit Order Drill-Through for Complex Orders

Default Drill-Through Protections will be applied to all complex limit and market orders that will cap the price of the

order relative to the SNBBO at the time of order entry. Exchange defaults are 5% through the contra-side of the

SNBBO. For orders other than SPX/SPXW, the price cap level will be no larger than $0.25 through the contra-side

SNBBO. For SPX/SPXW, the price cap will be no larger than $2.00 through the contra-side SNBBO. The price cap will

be no smaller than $0.02 through the contra-side SNBBO for all orders.

For complex orders not specifying a drill-through override with DrillThruProtection (FIX Tag 6253), the drill-through

mechanism will repeatedly post the order at a more aggressive price. If the order reaches its limit price at any time

during the iterative drill-through process, the order will remain at its limit price and the drill-through protection

mechanism will not continue. The preset duration is one second.

Sell market orders will drill through to the minimum tick for the class, where they will rest until cancelled or executed

in full. Buy market orders will drill through to the maximum allowable price for the class, where they will rest until

cancelled or executed in full. Market orders submitted with a TimeInForce of IOC will trade on arrival, capped at the

first drill-through price level.

Adjustments that would lock or invert an away displayed market will initiate a SUM auction. Eligible complex orders

may also initiate a COA throughout the iterative process.

Customers can optionally set more or less restrictive Drill-Through Protections on individual orders using

DrillThruProtection on the New Order Multileg message.

1.7.7.4 Exchange Default Fat Finger Limits

Fat Finger Checks are mandatory for both Pre-Market and Regular Sessions and applied to both simple and complex

orders. The following Exchange defaults are applied if not specified by the user. Fat Finger checks are not applicable

for any Multi-Class Spread instruments that trade on the floor only. Fat Finger checks are applicable for Multi-Class

complex instruments containing only SPX or SPXW legs as they are eligible for trading on the electronic book.

Pre-Open

Curb/GTH Session (VIX/XSP)

Limit Price Range

Fat Finger %

Default

Fat Finger Dollar-Based Limit

Default

$0.00 – $1.99

No Value

$1.00

$2.00 – $5.00

No Value

$1.50

$5.01 – $10.00

No Value

$2.00

$10.01 – $20.00

No Value

$3.00

$20.01 – $50.00

No Value

$4.00

$50.01 – $100.00

No Value

$6.00

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 14

$100.01 & Above

8%

Not Valid

Regular Session

Limit Price Range

Fat Finger %

Default

Fat Finger Dollar-Based Limit

Default

$0.00 – $1.99

No Value

$0.50

$2.00 – $5.00

No Value

$0.75

$5.01 – $10.00

No Value

$1.00

$10.01 – $20.00

No Value

$1.50

$20.01 – $50.00

No Value

$2.00

$50.01 – $100.00

No Value

$3.00

$100.01 & Above

4%

Not Valid

SPX and SPXW are considered Exception Classes and have unique Fat Finger default values for the Pre-Open and

Regular sessions.

Exception Class Pre-Open

Curb/GTH Session (SPX)

Limit Price Range

Fat Finger %

Default

Fat Finger Dollar-Based Limit

Default

$0.00 – $1.99

No Value

$15.00

$2.00 – $5.00

No Value

$15.00

$5.01 – $10.00

No Value

$15.00

$10.01 – $20.00

No Value

$15.00

$20.01 – $50.00

No Value

$20.00

$50.01 – $100.00

No Value

$20.00

$100.01 & Above

No Value

$25.00

Exception Class Regular Session

Limit Price Range

Fat Finger %

Default

Fat Finger Dollar-Based Limit

Default

$0.00 – $1.99

No Value

$1.00

$2.00 – $5.00

No Value

$1.50

$5.01 – $10.00

No Value

$2.00

$10.01 – $20.00

No Value

$3.00

$20.01 – $50.00

No Value

$4.00

$50.01 – $100.00

No Value

$6.00

$100.01 & Above

16%

Not Valid

See the Web Portal Port Controls Specification for additional details on how Members can manage fat finger settings

intraday.

1.7.7.5 Default Fat Finger Limits for Quote Updates

Quotes that cross the NBBO or displayed Cboe book will be accepted if within a configurable buffer range through

the NBBO or displayed Cboe book. The buffer is set to 5% with a minimum of $0.05 and a maximum of $1.00.

1.7.7.6 Maximum Open Order Limits

The exchange limits the maximum number of open orders allowed on a BOE or BOE Quote port to 200,000 per port.

New orders will be rejected once this limit is breached until the number of open orders drops back below 200,000.

Note this limit is only for orders and does not include open quotes sent over a BOE Quote port.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 15

1.7.8 Risk Root

This document uses the term “Risk Root” to describe Cboe Options Risk Management functionality that is applied at

the symbol-level. The Risk Root is defined as the underlying symbol. This impacts what value must be sent in the

defined RiskRoot fields when performing a mass cancel or a risk trip reset.

See the Risk Management Specification for more details.

1.7.9 Market Maker Trade Notifications (C1 Only)

Floor Trade Notifications (MMTNs) will be sent to Market Makers if they are identified as the contra party of a floor

trade. MMTN messages will be sent over a designated FIXDrop or BOE order entry port. See Section 10 – Port

Attributes section for information on available port attributes related to MMTNs.

Market Makers that receive a Floor Trade Notification should use the Floor Trade Confirmation message to respond

to the NNTN if they agree with the terms of the trade. Alternatively, a Market Maker can use the Add Floor Trade

message to enter their own version of the trade.

1.7.10 Cabinet and Sub-Cabinet Orders (C1 Only)

Cabinet orders are identified via PriceType = 0 and must have a valid TimeInForce of Day or GTC. Cabinet orders can

support a position status of Open or Close indentified via the OpenClose field. Cabinet orders will only trade with

other cabinet orders on the book or floor depending on FloorRoutingInst and FloorDestination values.

1.7.10.1 Valid Pricing

Orders in non-penny classes must have a limit price less than or equal to $0.01 and orders in penny classes must

have a limit price less than $0.01. Limit prices may be up to 4 decimal places.

1.7.10.2 Invalid Pricing

Orders in penny or non-penny classes priced greater than $0.01 and orders in penny classes priced equal to $0.01

will be rejected. Orders with a limit price that locks or crosses a resting non-cabinet order will be rejected.

1.7.10.3 Market Data

Cabinet orders or executions will not be disseminated on OPRA but will be available on

http://cdn.cboe.com/resources/membership/US_EQUITIES_OPTIONS_MULTICAST_PITCH_SPECIFICATION.pdf and

http://cdn.cboe.com/resources/membership/US_OPTIONS_MULTICAST_TOP_SPECIFICATION.pdf feeds.

1.7.11 Auction Orders

For more information on the following Auction Only Orders, please refer to the Opening Process Specification.

Order Type

Order Entry Details

Market-On-Open (MOO)

OrdType = 1 (Market)

TimeInForce = 2 (At the open)

Limit-On-Open (LOO)

OrdType = 2 (Limit)

Price = [price]

TimeInForce = 2 (At the open)

Settlement Liquidity On Open (SLOO)

OrdType = 2 (Limit)

Price = [price]

TimeInForce = 2 (At the open)

ExecInst = r (Settlement Liquidity)

1.7.12 Port Types

All BOE port types may be ordered using the Logical Port Request tool on the Customer Web Portal. Port attribute

changes may also be requested through this tool by submitting a ‘Modify’ request for one or more existing BOE

ports.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 16

1.7.12.1 BOE Order Ports

Standard BOE ports support simple and complex order entry but do not support the usage of Quote Update

message types and Purge Orders message types. The attempted usage of any of these message types on standard

BOE order ports will result in a rejection of the disallowed message.

Standard BOE ports are limited to 5,000 inbound messages per second. Once the inbound limit is reached new

orders are rejected, modifies are handled as cancels, and cancels are processed normally.

1.7.12.2 BOE Bulk Quoting Ports

BOE Bulk Quoting ports are intended for use by market makers quoting large numbers of simple options series. As

a result, they are unthrottled in terms of number of messages that may be accepted within any given period of time

from a TPH. However, market makers may still experience poor performance on Bulk Quoting ports if excessive

message traffic is sent.

The PreventMatch field may not be specified on the Quote Update message and Match Trade Prevention is only

available if defaulted at the port level. For Bulk Quoting ports, only Cancel Newest, Cancel Oldest, or Cancel Both

are permitted. If a Bulk Quoting port is not configured with both a default MTP Modifier and Unique ID Level, Match

Trade Prevention will be disabled.

Bulk Quoting Port Order Acceptance Table

Message

Simple/Complex

Accepted over Bulk

Quoting Port?

Other Conditions

Quote Update

Simple

Yes

Quote Update

(short)

Simple

Yes

New Order

Simple

Yes

Must have a TimeInForce value of Day

or GTD with a same day expiration on

C1, C2, and EDGX.

New Order

(Auction Response)

Simple

Yes

New Order Cross

(AIM or QCC)

Simple

No

New Order Cross

Multileg

Simple

No

Purge Orders

Simple/Complex

No

Reset Risk

Simple/Complex

Yes

New Complex

Instrument

Complex

Yes

Quote Update

Complex

No

New Complex

Order

Complex

Yes

Must be Post Only (RoutingInst = P).

Must have a TimeInForce value of Day

or GTD with a same day expiration on

C1, C2, and EDGX.

New Complex

Order

(COA Response)

Complex

Yes

Bulk Quoting Port Quote/Order Behavior Matrix

The following matrix describes the liquidity removal behavior of quotes and orders sent on Bulk Quoting ports. Bulk

Quoting ports are available for use by all customers but only Market Makers may use Quote Update messages.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 17

Orders sent on Bulk Quoting Ports are allowed to remove liquidity only on BZX Options. On C1, C2, and EDGX

Options, only registered Market Makers are allowed to remove liquidity using New Order messages.

Once a quote or order is posted to the exchange book, liquidity removal against any contra capacity is always allowed

in the case that a subsequent event causes the resting quote or order to be re-evaluated, such as the Opening/Re-

Opening Process.

• Only Market-Makers can send Quote Update messages, and such messages can only be sent on a Bulk

Quoting Port.

• Liquidity removal using either New Order or Quote Update messages on Bulk Quoting ports is restricted

to appointed Market-Makers only. Removal of any resting order with a Quote Update message by a

Market-Maker when not appointed in the class will result in a quoteResult reject of ‘r’ = Invalid Remove or

‘A’ = Market Maker must be registered for New Orders. For purposes of liquidity removal, an appointment

using any one EFID will allow for liquidity removal for all EFIDs used by the Market-Maker.

• New Order messages can be sent over FIX/BOE Ports and Bulk Quoting Ports by all capacities. However,

on C1, C2, and EDGX, non-Market-Maker New Order messages sent over a Bulk Quoting Port must be

marked “post only” and thus cannot remove liquidity.

Bulk Quoting Port

FIX/BOE Port

BZX

C2

EDGX

C1

BZX

C2

EDGX

C1

Can a Market-Maker send order

messages?

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Can a Market-Maker send quote

messages?

Yes

Yes

Yes

Yes

No

No

No

No

Can a non-Market-Maker send

order messages?

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Can a non-Market-Maker send

quote messages?

No

No

No

No

No

No

No

No

Can an aggressing Market-Maker

remove a resting Market-Maker

quote or order?

Yes

No

No

No

Yes

Yes

Yes

Yes

Can an aggressing Market-Maker

remove a resting non-Market-

Maker order?

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Can an aggressing non-Market-

Maker remove a resting Market-

Maker quote or order?

Yes

No

No

No

Yes

Yes

Yes

Yes

Can an aggressing non-Market-

Maker remove a resting non-

Market-Maker order?

Yes

No

No

No

Yes

Yes

Yes

Yes

1.7.12.3 BOE Purge Ports

BOE Purge Ports support a single Purge Orders message type. Members may use this port type to request a

cancellation of groups of orders, including orders across multiple BOE Order or Bulk Quoting ports.

1.7.13 Floor Routing (C1 Only)

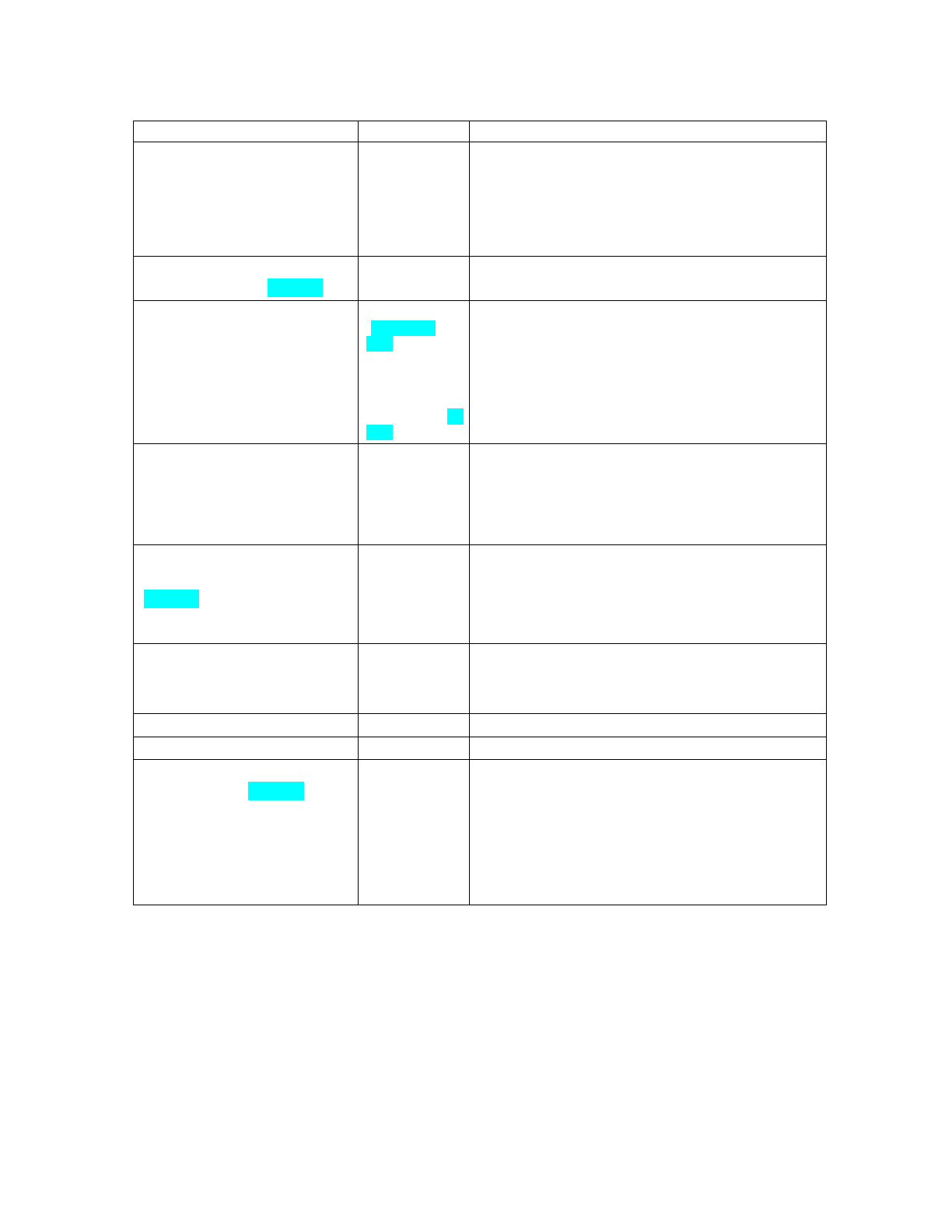

All orders routed to the floor must include explicit routing instructions that includes two features: 1) floor routing

instruction indicating Direct or Default routing behavior and 2) floor destination information. Floor routing behavior

is specified in FloorRoutingInst (22303). Direct routing sends the order to the indicated PAR workstation, while

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 18

default routing indicates that electronic execution is preferred, but the order may be routed to the indicated PAR if

it cannot be processed electronically.

Examples of conditions which cause default routing to the Floor include:

• a complex order having an AON contingency

• a complex order with multiple underlying components

• not held orders

Floor destination instructions are specified in FloorDestination (22100), indicating a PAR workstation (ex. W001) to

route to on the floor (or ‘PARO’ to rout to the Floor PAR Official of the underlying symbol) if not specified on the

inbound message. See Section 10 – Port Attributes for information on available port attributes, including Default

FloorRoutingInst and Default FloorDestination.

Order Tags/Port Settings

Handling of the Order

Order Floor

Destination

Order

FloorRoutingInst

Port

Default

Floor

Destination

Port Default

FloorRoutingInst

Orders Only

Executed on

Floor

(i.e. complex

AON)

All Other Order

Types

E (default)

Reject: ineligible

for electronic

book

Process

electronically

D

Reject: requires a

floor destination

Reject: requires a

floor destination

X

Reject: requires a

floor destination

Reject: requires a

floor destination

W001

E (default)

Reject: ineligible

for electronic

book

Process

electronically

W001

D

Route to floor:

W001

Route to floor:

W001

W001

X

Route to floor:

W001

Process

electronically

W009

E (default)

Reject: ineligible

for electronic

book

Process

electronically

W009

W001

D

Route to floor:

W009

Route to floor:

W009

W009

X

Route to floor:

W009

Process

electronically

W009

E

Reject: ineligible

for electronic

book

Process

electronically

W009

D

Route to floor:

W009

Route to floor:

W009

W009

X

Route to floor:

W009

Process

electronically

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 19

E

Reject: ineligible

for electronic

book

Process

electronically

D

Reject: requires a

floor destination

Reject: requires a

floor destination

X

Reject: requires a

floor destination

Process

electronically

E = Electronic only D = Direct X = Route to floor if unable to process electronically

1.7.13.1 Floor Representation Restatements (C1 Only)

Orders routed to the trading floor will be represented to the open outcry crowd before being traded in the crowd.

The Cboe BOE protocol provides a mechanism for clients to receive restatement of orders at the time of

representation.

BOE Floor Representation Restatements are sent to connected clients for each order when the floor broker reports

representation of the order to the crowd. Floor Representation Restatements sent to BOE ports will also be sent to

connected Order by Order Drop clients having the Floor Representation Restatements port attribute enabled.

Order Restated messages for floor representation will have RestatementReason = ‘F’ (Represented on Floor).

The TransactTime (60) will be the recorded time of the representation.

1.7.14 Stale NBBO

A stale NBBO will occur when the Cboe trading system determines that one or more SIP quote channels is impaired

or down completely. If the trading system detects that an NBBO is stale new orders for the affected class(es) will

be rejected. Any existing orders will remain on the book but will not be allowed to update (user updates or sliding

updates). Members will be allowed to cancel any open orders. Regular trading will resume when the NBBO for a

given class is determined to be healthy by the Cboe trading system.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 20

2 Session

2.1 Message Header Fields

Each message has a ten byte header. The two initial StartOfMessage bytes are present to aid in message reassembly

for network capture purposes. The MatchingUnit field is only populated on sequenced, non-session level messages

sent from Cboe to the Member. Messages from Member to Cboe and all session level messages must always set

this value to 0.

Field

Offset

Length

Data Type

Description

StartOfMessage

0

2

Binary

Must be 0xBA 0xBA.

MessageLength

2

2

Binary

Number of bytes for the message, including this

field but not including the two bytes for the

StartOfMessage field.

MessageType

4

1

Binary

Message type.

MatchingUnit

5

1

Binary

The matching unit which created this message.

Matching units in BOE correspond to matching

units on Multicast PITCH.

For session level traffic, the unit is set to 0.

For messages from Member to Cboe, the unit

must be 0.

SequenceNumber

6

4

Binary

The sequence number for this message.

Messages from Cboe to Member are sequenced

distinctly per matching unit.

Messages from Member to Cboe are sequenced

across all matching units with a single sequence

stream.

Member can optionally send a 0 sequence

number on all messages from Member to Cboe.

Cboe highly recommends that Members send

sequence numbers on all inbound messages.

2.2 Login, Replay and Sequencing

Session level messages, both inbound (Member to Cboe) and outbound (Cboe to Member) are unsequenced.

Inbound (Member to Cboe) application messages are sequenced. Upon reconnection, Cboe informs the Member of

the last processed sequence number; the Member may choose to resend any messages with sequence numbers

greater than this value. A gap forward in the Member's incoming sequence number is permitted at any time and is

ignored by Cboe. Gaps backward in sequence number (including the same sequence number used twice) are never

permitted and will always result in a Logout message being sent and the connection being dropped.

Most (but not all) outbound (Cboe to Member) application messages are monotonically sequenced per matching

unit. Each message's documentation will indicate whether it is sequenced or unsequenced. While matching units on

BOE correspond directly to matching units on Multicast PITCH, sequence numbers do not.

Upon reconnection, a Member sends the last received sequence number per matching unit in a Login Request

message. Cboe will respond with any missed messages. However, when the NoUnspeciedUnitReplay flag is enabled

in the Login Request message, Cboe will exclude messages from unspecified matching units during replay. Cboe

will send a Replay Complete message when replay is finished. If there are no messages to replay, a Replay

Complete message will be sent immediately after a Login Response message. Cboe will reject all orders during

replay.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 21

Assuming a Member has requested replay messages using a properly formatted Login Request message after a

disconnect, any unacknowledged orders remaining with the Member after the Replay Complete message is

received should be assumed to be unknown to Cboe.

Unsequenced messages will not be included during replay.

A session is identified by the username and session sub-identifier (both supplied by Cboe). Only one concurrent

connection per username and session sub-identifier is permitted.

If a login is rejected, an appropriate Login Response message will be sent and the connection will be terminated.

2.3 Sequence Reset

A reset sequence operation is not available for Binary Order Entry. However, a Member can send a Login Request

message with NoUnspecifiedUnitReplay field enabled, and NumberOfUnits field set to zero. Then, upon receiving a

Login Response message from Cboe, the Member can use the field LastReceivedSequenceNumber as the

sequence starting point for sending future messages.

2.4 Heartbeats

Client Heartbeat messages are sent from Member to Cboe and Server Heartbeat messages are sent from

Cboe to Member if no other data has been sent in that direction for one second. Like other session level messages,

heartbeats from Cboe to the Member do not increment the sequence number. If Cboe receives no inbound data or

heartbeats for 5 seconds, a Logout message will be sent and the connection will be terminated. Members are

encouraged to have a one second heartbeat interval and to perform similar connection staleness logic.

2.5 Logging Out

To gracefully log out of a session, a Logout Request message should be sent by the Member. Cboe will finish

sending any queued data for that port and will then respond with its own Logout message and close the connection.

After receipt of a Logout Request message, Cboe will ignore all other inbound (Member to Cboe) messages except

for Client Heartbeat messages.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 22

3 Session Messages

3.1 Member to Cboe

3.1.1 Login Request Message Fields

A Login Request message must be sent as the first message upon connection.

A number of repeating parameter groups, some of which may be required, are sent at the end of the message.

Ordering of parameter groups is not important. New parameter groups may be added in the future with no notice.

Field

Offset

Length

Data Type

Description

StartOfMessage

0

2

Binary

Must be 0xBA 0xBA.

MessageLength

2

2

Binary

Number of bytes for the message, including this

field but not including the two bytes for the

StartOfMessage field.

MessageType

4

1

Binary

0x37

MatchingUnit

5

1

Binary

Always 0 for inbound (Member to Cboe)

messages.

SequenceNumber

6

4

Binary

Always 0 for session level messages.

SessionSubID

10

4

Alphanumeric

Session Sub ID supplied by Cboe.

Username

14

4

Alphanumeric

Username supplied by Cboe.

Password

18

10

Alphanumeric

Password supplied by Cboe.

NumberOfParam

Groups

28

1

Binary

A number, n (possibly 0), of parameter groups to

follow.

ParamGroup

1

First parameter group.

…

ParamGroup

n

Last parameter group.

Unit Sequences Parameter Group

This parameter group includes the last consumed sequence number per matching unit received by the Member.

Cboe uses these sequence numbers to determine what outbound (Cboe to Member) traffic, if any, was missed by

the Member. If this parameter group is not sent, it's assumed the Member has not received any messages (e.g.,

start of day).

The Member does not need to include a sequence number for a unit if they have never received messages from it.

For example, if the Member has received responses from units 1, 3, and 4, the Login Request message need not

include unit 2. If the Member wishes to send a value for unit 2 anyway, 0 would be the only allowed value.

Only one instance of this parameter group may be included.

Field

Offset

Length

Data Type

Description

ParamGroupLength

0

2

Binary

Number of bytes for the parameter group, including

this field.

ParamGroupType

2

1

Binary

0x80

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 23

NoUnspecified

UnitReplay

3

1

Binary

Flag indicating whether to replay missed outgoing

(Cboe to Member) messages for unspecified units.

0x00 = False (Replay Unspecified Units)

0x01 = True (Suppress Unspecified Units Replay)

NumberOfUnits

4

1

Binary

A number, n (possibly 0), of unit/sequence pairs to

follow, one per unit from which the Member has

received messages.

UnitNumber

1

1

Binary

A unit number.

UnitSequence

1

4

Binary

Last received sequence number for the unit.

…

UnitNumber

n

1

Binary

A unit number.

UnitSequence

n

4

Binary

Last received sequence number for the unit.

Return Bitfields Parameter Group

This parameter group, which may be repeated, indicates which attributes of a message will be returned by Cboe for

the remainder of the session. This allows Members to tailor the echoed results to the needs of their system without

paying for bandwidth or processing they do not need.

Listing of the return bitfields which are permitted per message is contained in Section 7 – Return Bitfields per

Message.

Field

Offset

Length

Data Type

Description

ParamGroupLength

0

2

Binary

Number of bytes for the parameter group,

including this field.

ParamGroupType

2

1

Binary

0x81

MessageType

3

1

Binary

Return message type for which the bitfields are

being specified (e.g., 0x25 for an Order

Acknowledgment message).

NumberOfReturn

Bitfields

4

1

Binary

Number of bitfields to follow.

ReturnBitfield

1

5

1

Binary

Bitfield identifying fields to return.

…

ReturnBitfield

n

1

Binary

Last bit field.

Cboe Options Exchanges

BOE Specification (Version 2.11.67)

© 2024 Cboe Global Markets, Inc. or one or more of its affiliates.

All Rights reserved 24

Login Request Message Example

Note this example is for illustrative purposes only. Actual login messages will contain specification of return bitfields

for a larger set messages and each return bitfield specification will be complete whereas the example below is only

an illustration for purposes of demonstrating the construction of the Login Request message.

Field Name

Hexadecimal

Notes

StartOfMessage

BA BA

Start of message bytes.

MessageLength

3D 00

61 bytes

MessageType

37

Login Request

MatchingUnit

00

Always 0 for inbound messages

SequenceNumber

00 00 00 00

Always 0 for session level messages

SessionSubID

30 30 30 31

0001

Username

54 45 53 54

TEST

Password

54 45 53 54 49 4E 47 00 00 00

TESTING

NumberOfParam

Groups

03

3 parameter groups

ParamGroupLength

0F 00

15 bytes for this parameter group

ParamGroupType

80

0x80 = Unit Sequences

NoUnspecified

UnitReplay

01

True (replay only specified units)

NumberOfUnits

02

Two unit/sequence pairs to follow;

UnitNumber

1

01

Unit 1

UnitSequence

1

4A BB 01 00

Last received sequence of 113,482

UnitNumber

2

02

Unit 2

UnitSequence

2

00 00 00 00

Last received sequence of 0

ParamGroupLength

08 00

8 bytes for this parameter group

ParamGroupType

81

0x81 = Return Bitfields

MessageType

25

0x25 = Order Acknowledgment

NumberOfReturn

Bitfields

03

3 bitfields to follow

ReturnBitfield

1

00

No bitfields from byte 1

ReturnBitfield

2

41

Symbol, Capacity

ReturnBitfield

3

05

Account, ClearingAccount