A Simple Guide To Your

FINANCIAL

STATEMENTS

Understanding

Where You Stand:

Illinois Small Business Development Centers

"Experts, networks, and tools to transform your business"

Illinois Small Business Development Centers

(SBDC) provide information, confidential

business guidance, training and other

resources to early stage and existing small

businesses.

Illinois International Trade Centers (ITC)

provide information, counseling and

training to existing, new to-export

companies inte

rest

ed in pursuing

international trade opportunities.

Illinois Procurement Technical

Assistance Centers (PTAC) provide one-

on-one counseling, technical

information, marketing assistance and

training to existing businesses

that are interested in selling their

products and/or services to

local, state, or federal

government agencies.

Technology, Innovation and

Entrepreneurship Specialty

(TIES) ten SBDC location

s

help

Illinois businesses,

entrepreneurs and citizens to

succeed in a changing economy by:

developing the skills of their workers;

promoting safe and healthy workplaces;

assisting in the commercialization of new

technologies; and providing access to

modernizing technologies and practices.

Jo Daviess

Stephenson

Winnebago

Boone Mc Henry Lake

Carroll

Ogle

De Kalb

Kane

Cook

Du Page

Whiteside

Lee

Kendall

Rock Island

Henry

Bureau

Putnam

La Salle

Grundy

Will

Kankakee

Livingston

Mercer

Henderson

Warren

Knox

Stark

Marshall

Hancock

Mc Donough

Fulton

Peoria

Woodford

Tazewell

McLean

Ford

Iroquois

Adams

Schuyler

Brown

Cass

Menard

Logan

De Witt

Piatt

Champaign

Vermilion

Edgar

Douglas

Moultrie

Macon

Christian

Sangamon

Morgan

Scott

Pike

Calhoun

Greene

Macoupin

Jersey

Montgomery

Shelby

Coles

Clark

Cumberland

Madison

Bond

Fayette

Engham

Jasper

Crawford

St. Clair

Clinton

Marion

Clay

Richland

Lawrence

Monroe

Ra

ndolph

Perry

Washington

Jeerson

Wayne

Edwards

Wabash

Jackson

Franklin

Hamilton White

Williamson

Saline Gallatin

Union

Johnson

Pope

Hardin

Alexander

Pulaski

Massac

Mason

www.ilsbdc.biz

Business Center Locations

SBDC

SBDC/ITC

SBDC/ITC/PTAC

SBDC/PTAC

PTAC

Technology Services

*

See Northeast Region map on other side

for Business Center Services in that area.

*

See

Note

Below

800-252-2923

This resource is made possible through a partnership with the Illinois Department of Commerce and Economic

Opportunity, Small Business Development Center and the U.S. Small Business Administration.

*See the Northeast Region map on the last page

for the Business Center Services in that area.

See

Note

Below

B A L A N C E

S H E E T

I N C O M E

S TAT E M E N T

C A S H F L O W

S TAT E M E N T

R AT I O S

10

8

6

4

I N T R O D U C T I O N

One statement cannot diagnose your company’s financial health. Put several

statements together and you can make smart financial, investment and

management decisions.

Many business owners don’t know how to read their statements and rely on

advisors (such as accountants) to tell them the results. Their input is valuable

b

ut you need to educate yourself. You must be able to understand your

statements so you can:

realize the vital role money plays in every business decision

determine if you are making a profit or losing money

calculate your current and future financial needs:

make sure you have positive cash flow for short-term needs

make sure your business is growing and will continue to grow

For lending purposes, statements will help you determine:

if you can afford to pay a loan

the loan amount

the loan term (number of years)

which assets you should buy vs. which assets should be financed

what collateral is available to secure a loan

W H AT A R E T H E S E S TAT E M E N T S ?

Financial statements are meaningful, written records which allow you to diagnose

your financial strengths and weaknesses and increase the life and profitability of

your company. Statements are usually prepared annually although the income

statement should be developed on a monthly or, at least, a quarterly basis.

W H AT D O T H E S E STAT E M E N T S SHO W ?

Balance Sheet

What a company owns, what it owes, and what is left over.

Income Statement

A firm’s sales and expenses plus its profit (or loss).

Ratios

Analyze a company’s financial condition. Ratio answers can be compared

to others in the same industry.

Cash Flow Statement

The sources, uses, and balance of cash, shown on a monthly basis.

3

CC oo nn tt ee nn tt ss

U N D E R S T A N D I N G W H E R E Y O U S T A N D

NewGround Publications. (Phone: 800 207-3550) All rights reserved. Photocopying any part of this book is against the law.

This book may not be reproduced in any form, including xerography, or by any electronic or mechanical means, including information

storage and retrieval systems, without prior permission in writing from the publisher. 0211

BALANCE SHEETS:

BEFORE AND AFTER

FINANCING

Established

companies should

develop two Balance

Sheets - one before,

and one the day after

the loan closes.

New companies

should include an

opening Balance Sheet

in the projections to

reflect what the

balance sheet

will look like the day

after the loan closes.

BB aa ll aa nn cc ee

SS hh ee ee tt

4

U N D E R S T A N D I N G W H E R E Y O U S T A N D

Liabilities + Net Worth = Assets

Think of the Balance Sheet like a scale. Assets and liabilities alone are

out of balance until you add capital, the last weight put on the scale, to

makes it balance.

Assets

Assets are divided into two categories: current and

non-current. They are listed according to how liquid

they are (how quickly they can be turned into cash).

Examples of current assets are cash and inventory.

Examples of non-current assets are

furniture, fixtures,

property and equipment

. Money owed to your

company (accounts receivable) is considered an asset.

Liabilities

Liabilities (debts you owe) are divided into two categories: current and

non-current (or long-term). They are listed in the order they need to be repaid.

Capital or Net Worth

The business’ equity includes money the owners have invested and income

kept in the business from the company’s profits.

W H AT I T S H O W S Y O U

The net value of the business

How much of your loan debt is current, and how much is long-term

Percentages and ratios (which are extracted from the numbers)

necessary to analyze your business (see Ratios section)

Compare two of the same time periods to see changes in:

cash accounts payable accounts receivable

equity inventory retained earnings

W H AT I T W O N ’ T S H O W Y O U :

Income or expenses over a period of time.

Remember, the Balance Sheet reflects one moment in time.

Market value of assets, although it will reflect purchase costs and

depreciation according to industry standards

Quality of assets

Contingent Liabilities (money you agreed to repay by signing notes,

or by being a co-maker or guarantor of loans).

Operating Lease obligations (which allow you to buy the item at the end

of the lease, for a set price, do not appear on the Balance Sheet). However,

Capital Leases (with buyout price of $1) are shown on the Balance Sheet.

ASSE

T

S

LIABILITIES

+

CAPITAL

ASSETS

W H AT D O E S A B A L A N C E S H E E T T E L L Y O U ?

This statement shows what you own (assets), what you owe (liabilities), and

what’s left over (net value or equity in the business). The numbers change every

time you receive money or give credit to a client as well as when you pay for or

charge an expense.

The Balance Sheet is

a picture of your

business, frozen for a

second in time.

L

I

A

B

I

L

I

TI

E

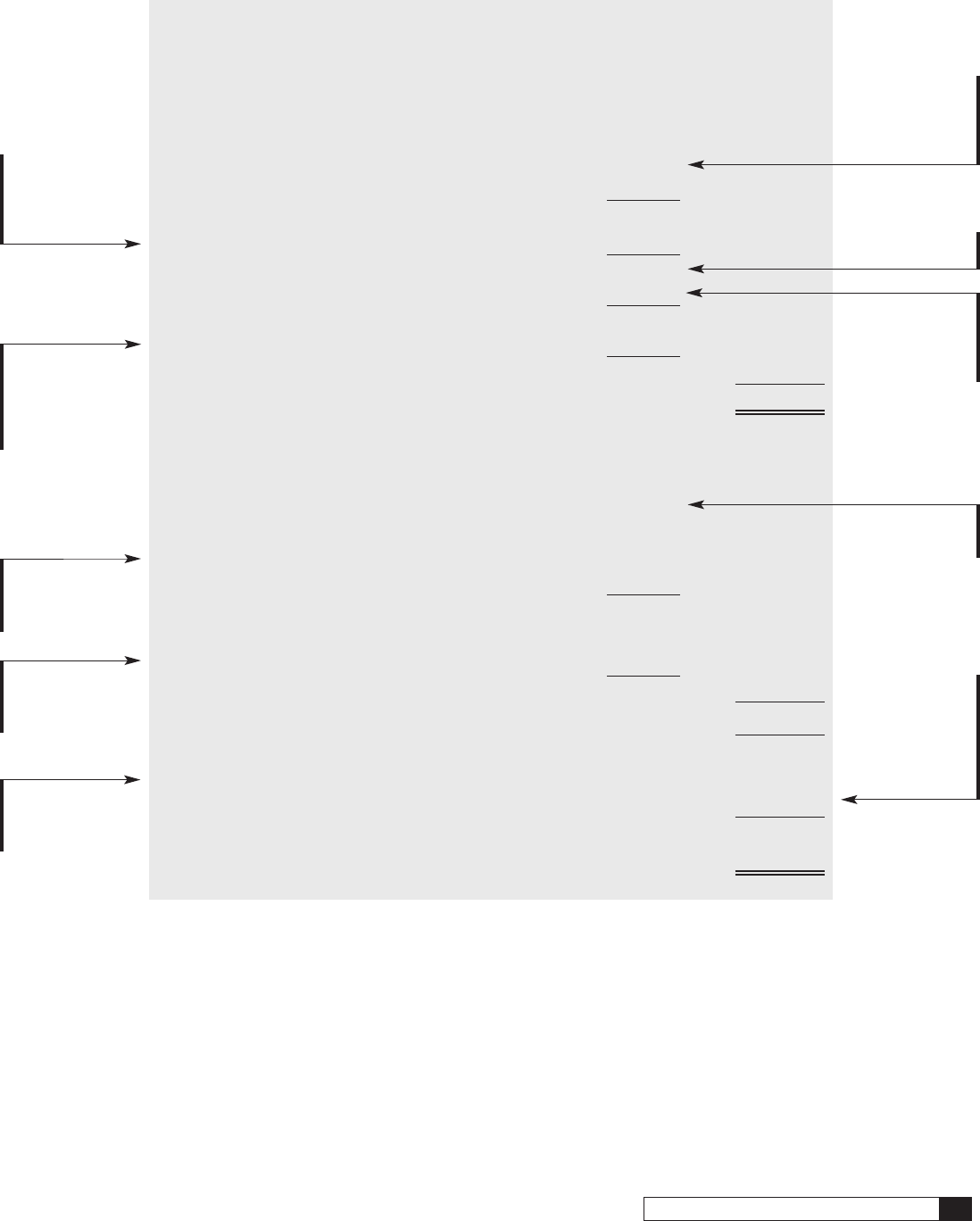

S

Max Computer Company, Balance Sheet

ASSETS

(WHAT YOU OWN)

Current Assets (converts to cash in one year)

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,000

Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75,000

I

nventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85,000

Total Current Assets (10K+75K+85K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170,000

Non-Current Assets (more than one year to convert to cash)

Fixed Assets (furniture, fixtures, property, equipment) . . . . . . . . . 140,000

Less Accumulated Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . - 25,000

Fixed Assets (net, 140K - 25K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115,000

Advances to Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,000

Total Non-Current Assets (115K + 6K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121,000

Total Assets (170K + 121K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291,000

LIABILITIES

(WHAT YOU OWE)

Current Liabilities (due within one year)

Accounts Payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41,000

Accrued Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,000

Current Portion of Long-Term Debt . . . . . . . . . . . . . . . . . . . . . . . . . . 6,000

Note Payable (due within one year) . . . . . . . . . . . . . . . . . . . . . . . . .100,000

Total Current Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .150,000

Long-Term Liabilities (due for more than one year)

Loan Payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54,000

Total Long Term Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54,000

Total Liabilities (150K + 54K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 204,000

CAPITAL OR NET WORTH

(THE COMPANY’S EQUITY)

Owners Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20,000

Retained Earnings (income kept in the business) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67,000

Total Capital or Net Worth (67K + 20K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87,000

Total Liabilities & Capital (204K + 87K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291,000

Depreciation

Assets lose their

value. Deductions

are made according

to tax rules

Current Portion

of Long-Term Debt

One year’s worth of

loan payments

Accounts

Receivable

Sales made but

money still owed to

the company

Advances to

Owners

Money owners

take, in the form

of a loan, to be

repaid

Loan Payable

Loan balance after

one year’s worth

of payments

Non-Current

Assets

Takes more than

one year to turn

into cash

Owners

Investment

Money owners

invest in business

THE CASH METHOD

Records a sale when

money is collected

Records an expense

when it is paid

5

U N D E R S T A N D I N G W H E R E Y O U S T A N D

W H I C H A C C O U N T I N G M E T H O D I S R I G H T F O R Y O U

THE ACCRUAL METHOD

Sales are made on credit, and not immediately paid for.

The amount customers owe is called Accounts Receivable

Buy items or incur expenses for the business, but pay later.

The amount owed is called Accounts Payable.

Net worth does not always translate to cash, since money can be tied up in

Accounts Receivable, expenses and inventory. To get a better idea of how much

cash there is at the end of the month, learn about the Cash Flow Statement.

Lenders prefer the accrual method.

Retained Earnings

Money left in the

business from the

company’s profits,

accumulated over

the life of the

business.

Accounts Payable

Purchases not

paid for

Fixed Assets

Original Cost

Think of the

Income Statement

as a report card

for your business.

It is issued from

time to time

and gives an

overview of how

you are doing.

II nn cc oo mm ee

SS tt aa tt ee mm ee nn tt

6

U N D E R S T A N D I N G W H E R E Y O U S T A N D

W H AT D O E S A N I N C O M E S TAT E M E N T T E L L Y O U ?

In the day-to-day running of your business, numbers fly around at a dizzying

pace. Bills are paid, money is taken in, and sometimes, in this whirlwind of

activity, it’s hard to know how much you’re actually making. The Income

Statement answers that question.

Think of the Income Statement as a kind of report card for your business.

Like a report card, it is issued from time to time and gives an overview

of how you are doing (for that period of time).

Since this statement reflects your business activity over time (not like the Balance

Sheet which is a snapshot of your business for one moment in time), it is usually

developed monthly, quarterly and annually. Creating a projected statement for

the next 12 months, based on your predictions, is also a good idea.

W H AT I T S H O W S Y O U

If sales are going up or down

Your gross profit — how much money is left for the rest of the business

after deducting what it costs to produce or purchase the product

All expenses for the time period it covers

Increases and decreases in net income

How much money is left to grow the business

How much money is left for the owner(s)

How much money is left to pay debt (principal only)

W H AT I T W O N ’ T S H O W Y O U

If your overall financial condition is weak or strong (see the Balance Sheet).

What’s tied up in Accounts Receivable (money owed to you) and

Accounts Payable (money you owe).

What you own (assets) and what you owe (liabilities)

O T H E R NAM E S F O R T H I S S TAT E M E N T

• Operating Statement • Earnings Statement • Profit & Loss Statement (P&L)

To get a more accurate picture of your financial performance,

compare percentages instead of numbers.

First, convert numbers from the Income Statement into percentages

Next, compare these percentages from this period to those from the

previous period

Are the percentages increasing or decreasing?

F O R E X A M P L E

7

U N D E R S T A N D I N G W H E R E Y O U S T A N D

Max Computer Company, Income Statement

Net Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .900,000 100%

Less Cost of Goods Sold (cost to make products):

Beginning Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75,000 8%

P

urchases (to make product) . . . . . . . . . . . . . . . . . . . . . . . . 350,000 39%

Labor (to make product only) . . . . . . . . . . . . . . . . . . . . . . . 200,000 22%

Total (75K+350K+200K) . . . . . . . . . . . . . . . . . . . . . . . . . . . 625,000 69%

Less: Ending Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . - 85,000 9%

Cost of Goods Sold (625K less 85K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 540,000 60%

Gross Profit (900K less 540K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 360,000 40%

Operating Expenses:

Selling Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90,000 10%

General and Administrative . . . . . . . . . . . . . . . . . . . + 170,000 19%

Total Expenses (90K + 170K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 260,000 29%

Operating Income (360K less 260K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100,000 11%

Less: Interest Expense (on loans) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . - 20,000 2%

Net Profit before taxes (100K less 20K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80,000 9%

Less: All Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . - 27,000 3%

Net Profit (80K less 27K) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53,000 6%

Net Profit

Profit left after all

expenses have

been paid

Gross Profit

This is your

profit margin

Selling Expenses

Salaries and

expenses related

to sales only

General & Admin-

istrative

All other expenses

used to run the

company

Operating Income

(or Loss)

Shows how the

business performed

Gross Profit of $360,000

Total Sales of $900,000

=

40%

If gross profit was 35% last year, it has increased by 5%

Net Sales

Revenue or income.

Gross sales is

before returns

and allowances.

Net sales is after

returns and

allowances.

W H AT D O E S A C A S H F L O W S TAT E M E N T T E L L Y O U ?

Cash is the fuel that runs your business. Running out of it would be disastrous, so

you must have a “cash flow” or money on hand to pay bills and meet day-to-day

expenses. Keep in mind that companies can produce a profit, but still not have a

positive cash flow.

The Cash Flow Statement shows money that comes into the business, money that

goes out and money that is kept on hand to meet daily expenses and emergencies.

W H AT I T S H O W S Y O U

If the business has enough money to:

- cover day-to-day activities

- pay debts on time

- maintain and grow the business without a negative cash flow

The need for additional working capital (cash) when sales increase since

increased sales mean increased purchases of material or labor. You should

know how much you need. Show where the additional working capital will

come from.

The maximum loan payment the business can afford

The breakdown of principal and interest on your loan payments.

Note that the Income Statement only shows interest - not principal.

Your weaknesses (an inability to keep and generate cash). For lending

purposes, explain how you’ll handle these weaknesses (via increased

sales, cost reductions, or owner’s investments).

W H AT I T W O N ’ T S H O W Y O U

How much you have in Accounts Receivable and Accounts Payable

(shown in the Balance Sheet)

Your balances in assets, liabilities and net worth

Depreciation of equipment, which is a non-cash expense.

This is dealt with in the Balance Sheet.

CC aa ss hh FF ll oo ww

SS tt aa tt ee mm ee nn tt

8

U N D E R S T A N D I N G W H E R E Y O U S T A N D

Of Special Interest to New Companies

Losses - also called “pull down balances” - are common

in the first year of a start-up. Lenders want to see the

business break-even during the year. To produce positive

balances, you’ll have to cover months (that show negative

balances) with loans, increased revenue, additional

owner’s investments, or by reducing expenses.

What money comes

in, what goes out,

and what stays

9

U N D E R S T A N D I N G W H E R E Y O U S T A N D

J

J

a

a

n

n

F

F

e

e

b

b

M

M

a

a

r

r

A

A

p

p

r

r

i

i

l

l

M

M

a

a

y

y

J

J

u

u

n

n

e

e

J

J

u

u

l

l

y

y

A

A

u

u

g

g

S

S

e

e

p

p

t

t

O

O

c

c

t

t

N

N

o

o

v

v

D

D

e

e

c

c

T

T

o

o

t

t

a

a

l

l

A

A

.

.

C

C

a

a

s

s

h

h

O

O

n

n

H

H

a

a

n

n

d

d

(

(

B

B

e

e

g

g

i

i

n

n

n

n

i

i

n

n

g

g

o

o

f

f

m

m

o

o

n

n

t

t

h

h

)

)

1

1

0

0

,

,

0

0

0

0

0

0

5

5

,

,

6

6

2

2

7

7

1

1

3

3

,

,

7

7

4

4

1

1

1

1

0

0

,

,

4

4

7

7

0

0

1

1

3

3

,

,

8

8

3

3

0

0

1

1

5

5

,

,

1

1

9

9

0

0

1

1

1

1

,

,

4

4

9

9

8

8

1

1

5

5

,

,

2

2

0

0

2

2

2

2

2

2

,

,

1

1

5

5

7

7

3

3

0

0

,

,

9

9

9

9

7

7

3

3

9

9

,

,

3

3

7

7

2

2

4

4

8

8

,

,

6

6

0

0

1

1

B. Cash Receipts

1. Cash Sales

2. Collections from Credit Accounts 32,813 75,000 76,250 81,250 85,000 85,750 88,500 90,000 88,750 84,250 81,500 78,750

3. Loan or Other Cash injection (specify)

C. Total Cash Receipts (B1+B2+B3) 32,813 75,000 76,250 81,250 85,000 85,750 88,500 90,000 88,750 84,250 81,500 78,750

D. Total Cash Available (A+C, before cash paid) 42,813 80,627 89,991 91,720 98,830 100,9 40 99,998 105,202 110,907 115,247 120,872 127,351

E. Cash Paid Out:

1. Purchases (Merchandise) 0 30,000 42,500 42,500 44,000 45,000 45,000 42,500 41,000 40,000 37,500 37,500 447,500

2. Gross Wages (excludes withdrawals) 10,758 10,758 11,364 11,970 11,970 12,334 12,576 12,576 11,970 11,606 11,364 10,758 140,004

3. Payroll Expenses (Taxes, etc.) 1,076 1,076 1,136 1,197 1,197 1,233 1,258 1,258 1,197 1,161 1,136 1,076 14,001

4. Outside Services 758 758 808 859 859 889 909 909 859 828 808 758 10,002

5. Supplies (Office and operating) 383 383 408 434 434 449 459 459 434 418 408 303 4,972

6. Repairs and maintenance 390 390 416 422 422 458 468 468 442 426 416 390 5,108

7. Advertising 4,200 4,200 4,200 4,200 4,200 4,200 4,200 4,200 4,200 4,200 4,200 4,200 50,400

8. Car, Delivery and Travel 2,700 2,700 2,800 2,900 2,900 2,960 3,000 3,000 2,900 2,840 2,800 2,700 34,200

9. Professional Services (Accounting, legal, etc.) 1,500 001,500 000001,500 004,500

10. Rent 1,950 1,950 1,950 1,950 1,950 1,950 1,950 1,950 1,950 1,950 1,950 1,950 23,400

11. Telephone 278 278 296 315 315 326 333 333 315 303 296 278 3,666

12. Utilities 400 400 400 400 400 400 400 400 400 400 400 400 4,800

13. Insurance 0 450 450 450 450 450 450 450 450 450 450 0 4,500

14. Taxes (real estate, etc.) 0 750 00750 00750 00750 0 3,000

15. Interest (on loans) 500 498 495 493 490 488 485 482 480 477 475 472 5,835

16. Other/Miscellaneous Expenses (specify) 0000000000000

17. Subtotal 24,893 54,591 67,223 69,590 70,337 71,137 71,488 69,735 66,597 66,559 62,953 60,785 755,888

F. Other Operating Costs:

1. Loan Principal Payment 293 295 298 300 303 305 308 310 313 316 318 321 3,359

2. Capital Purchases (ex., Buy a computer) 000005,000 00 00005,000

3. Other Start-up Costs 0000000000000

4. Reserve and/or Escrow (ex., Pay $100K loan) 10,000 10,000 10,000 5,000 10,000 10,000 10,000 10,000 10,000 5,000 5,000 5,000

100,000

5. Owner’s Withdrawal 2,000 2,000 2,000 3,000 3,000 3,000 3,000 3,000 3,000 4,000 4,000 4,000 36,000

G. Total Cash Paid Out (E17 + F1 through F5) 37,186 66,886 79,521 77,890 83,640 89,442 84,796 83,045 79,910 75,875 72,271 70,106

H. Cash Position (End of month, D minus G) 5,627 13,741 10,470 13,830 15,190 11,498 15,202 22,157 30,997 39,372 48,601 57,245

I. Essential Operating Data (Non-cash flow info)

1. Accounts Receivable (End of month) 117,188 117,188 120,938 124,688 124,688 126,938 128,438 128,438 124,688 122,438 120,938 117,188

2. Bad Debt (End of month, if applicable) 000000000000

3. Inventory on Hand (End of month) 77,500 82,500 85,000 86,500 89,000 90,000 87,500 83,500 81,000 77,500 75,000 75,000

4. Accounts Payable (End of month) 71,000 83,500 83,500 85,000 86,000 86,000 83,500 82,000 81,000 78,500 78,500 78,500

Loan Payment

Loan received a month before these

projections. Purchases are paid,

up to date. They are now taking

advantage of 30-day payment

terms. The Income Statement

will record the purchases as an

Accounts Payable but it won't be

recorded here until paid.

Loan Principal

Loan principal appears here but

not in the Income Statement. If

the loan was used for real estate,

furniture, fixtures and equipment

or machinery, that portion will

be depreciated over time (as

allowed by the IRS) on the

Income Statement.

Cash Position

This company has

a positive cash flow.

Summary

Good information

to calculate

F O R M U L A

F

O R M U L A

F O R M U L A

F O R M U L A

L I Q U I D I T Y R AT I O S

How “cash rich” is a company?

Liquidity ratios show a company’s

ability to turn an asset into cash.

QUICK OR ACID TEST RATIO

Number Source: Balance Sheet

N O T E : This shows how many days it takes to

collect money owed to you.

Lower answer is better.

A S S E T M A N A G E M E N T

R AT I O S

How effectively are you

managing your assets?

INVENTORY TURNOVER

Number Source: Balance Sheet

& Income Statement

N

O T E :

Shows if a company has enough cash to

pay bills. This example shows an excess amount

after paying all current liabilities. The answer

must be positive. More money is needed to meet

expenses if the answer is a negative number.

Higher number is better.

N O T E : This formula shows how many days it

takes you to turnover (or sell) your inventory.

Lower answer is better.

Total Current Assets of $170,000

less Inventory of $85,000

Eliminates

inventory

from current

assets

and cash.

“Quick” means

items can

be turned

into cash.

Total Current Liabilities

$27,375,000

$900,000

=

30.4

Accounts Receivable

($75,000 x 365 days)

Net Sales Figure

I

t takes

30 days

to collect

b

ills

$31,025,000

$540,000

=

57.4

Inventory Figure

($85,000) x 365 days

Cost of Goods Sold

57 days to

turnover or

sell the in-

ventory

$170,000

- $150,000

=

$20,000

Current Assets

Subtract Current Liabilities

ACCOUNTS RECEIVABLE TURNOVER

Number Source: Balance Sheet

& Income Statement

$85,000

$150,000

=

.56

N O T E : Inventory may become no longer useful.

This ratio eliminates inventory from current

assets and cash. It’s called “quick” because it

includes items that can be turned into cash.

Answer should be 1 or higher.

N O T E : Tests a company’s short-term debt

paying ability. This means there is is $1.13 in

cash and current assets available to pay every

$1 of current liabilities.

The higher the number, the better.

Answer should be 2 or more

$170,000

$150,000

=

1.13

Total Current Assets

Total Current Liabilities

CURRENT RATIO

Number Source: Balance Sheet

Think of ratios as

your business’

financial scores

RR aa tt ii oo ss

10

U N D E R S T A N D I N G W H E R E Y O U S T A N D

F

O R M U L A

WORKING CAPITAL

Nu mber Source: Balance Sheet

A company’s

short-term

debt paying

ability.

Shows if

a

company

has enough

cash to

p

ay bills.

Answer

must be

p

ositive

W H AT R AT I O S S H O W Y O U ?

Ratios help you identify your strengths and

weaknesses. Use them to compare your

business to standards in your industry.

Lenders look very carefully at ratios.

The numbers for ratios are taken from the

Income Statement and the Balance Sheet,

but not the Cash Flow Statement.

F O R M U L A

F O R M U L A

F O R M U L A

F O R M U L A

CASH FLOW TO CURRENT MATURITIES

(DEBT SERVICE) RATIO

Number Source: Balance Sheet

& Income Statement

PROFIT MARGIN ON SALES

Number Source: Income Statement

ACCOUNTS PAYABLE TURNOVER

Number Source: Balance Sheet

& Income Statement

LEVERAGE (OR DEBT TO WORTH) RATIO

Number Source: Balance Sheet

NO T E : Shows how quickly a company pays its suppliers.

Lower numbers (30 days or less) are better.

N O T E : Shows the percentage of net profit for every

dollar of sales. The higher the number, the better.

If the profit margin is too low:

1. the prices are too low

2. the cost of goods is too high

3. expenses are too high

Note: Shows your ability to pay term debts after

owner(s) withdrawals. New businesses, use

one year's worth of loan payments.

Answer of 2 or more is preferred.

N

O T E :

Determines if a company has enough equity.

Lower answers are better.

Answer of 3 or lower is preferred.

$204,000

$87,000

=

2.34

T

otal Liabilities

T

otal Capital

T

he company

is leveraged

2.34 times.

F

or every $1

owners have

invested,

l

enders and

creditors

have invested

$

2.34

$53,000

$900,000

=

.0588

Net Profit

N

et Sales

The

profit

m

argin

is 5.9%

$66,000

$6,000

=

$11

N

et Profit of $53,000 + Depreciation of

$13,000 (amount created for this example)

Current Portion of

Long Term Debt.

F

or every

dollar of

payments

$

11 is

available to

pay it

$14,965,000

$350,000

=

42.75

Accounts Payable at

$

41,000 x 365 days

Purchases

Accounts

P

ayable

are paid

every

4

3 days

D E B T M A N A G E M E N T R AT I O S

Shows how much money owners have

invested in the business versus lenders.

P R O F I TA B I L I T Y R ATI O S

Shows company’s ability to make a profit

R

atio Comparisons

Ratios should be

compared to prior

years, acceptable

lending ranges, and

industry averages.

Industry ratios are averages.

Some firms are above and

some firms are below these

numbers. Differences are due

to the age of the company,

locations, managers, and

operations, to name a few.

A ratio of 38% compared to

an industry average of 39%

seems like a small 1%

difference. If sales are $4

million, 1% is $40,000.

If net profits are $100,000,

then the $40,000 is very

important.

These reference books

include industry

information:

RMA Annual

Statement Studies

Almanac of Business and In-

dustrial Financial Ratios

(gathered from U.S. Treasury

and IRS information)

Dunn and Bradstreet

Other good industry

sources (especially

when your company

is smaller than those

used in the reference

books):

Trade Associations

Magazines and newspapers

for your industry

Small Business Administra-

tion/SBA

R AT I O S AT A G L A N C E

R A T I O G E T N U M B E R S F R O M :

A S S E T M A N AGE M E N T

Accounts Receivable Turnover . . . . . . . .Balance Sheet & Income Statement

Inventory Turnover . . . . . . . . . . . . . . . . .Balance Sheet & Income Statement

L I Q U I D I T Y RAT I O S

Working Capital . . . . . . . . . . . . . . . . . . . .Balance Sheet

Quick or Acid Test . . . . . . . . . . . . . . . . .Balance Sheet

Current . . . . . . . . . . . . . . . . . . . . . . . . . .Balance Sheet

D E B T M A N A GEME N T R AT I OS

Leverage (or Debt to Worth) . . . . . . . . . .Balance Sheet

Accounts Payable Turnover . . . . . . . . . .Balance Sheet & Income Statement

P R O F I TA B I L I T Y

Profit Margin on Sales . . . . . . . . . . . . . . .Income Statement

Cash Flow to Current

Maturities (Debt Service) . . . . . . . . . . . .Balance Sheet

11

U N D E R S T A N D I N G W H E R E Y O U S T A N D

Ability to Pay.

Ability to pay loans from future

business’ profits.

Accounts Payable (A/P).

Expenses incurred from

purchases made on credit.

Accounts Receivable (A/R).

Sales

m

ade but money not collected. Credit is granted.

Assets.

What a company owns.

Asset-based Lending.

Financing secured by pledging

assets (inventory, receivables, or other collateral).

Available Credit.

The unused portion of a line of credit.

Balloon.

A stop point or early maturity of a loan.

Business Credit.

Loans made to businesses in the form

of a term loan or a line of credit.

Business Plan.

An overview of a new or existing

company which is used to obtain financing.

Capacity.

Borrower’s ability to handle a certain level

of debt.

Capital Leases.

Leases with a buyout price of $1 which

are shown on the Balance Sheet.

Commercial Mortgage.

A loan on business’ real estate.

Rates and terms are negotiated and the interest rate

is usually related to the prime rate.

Cost of Goods Sold.

Cost to make a product, including

materials, labor, and related overhead.

Credit Rating.

Credit rating as determined by a credit

reporting agency.

Credit Scoring.

A process used to approve or reject

commercial loan applications, based on ratios and

other factors.

Current Assets.

Assets that can be converted into cash

in one year.

Current Liabilities.

Liabilities due within one year.

Depreciation.

Except for land, assets wear out.

They are devalued or depreciated every year.

Draw Down.

Taking an advance on a line of credit.

Equity.

The book value of a business.

Assets minus liabilities.

Fair Market Value (FMV).

The price of an asset,

product or service in a current, competitive market.

Fixed Assets.

Assets including furniture, fixtures,

equipment, machinery, and real estate.

Gross Profit.

Gross sales less cost of goods sold.

Also called gross margin.

Gross Sales.

Revenue or income from sales before

returns and allowances.

Intangible Asset.

Have no physical properties but

represent something of value (for example, patents

and trademarks).

Inventory.

Assets held for resale. May be in the form of

raw materials, work in progress, or finished goods.

Liquid Collateral.

Collateral that can be converted to

cash quickly.

Line of Credit (LOC).

A short-term loan (usually used

to finance accounts receivable and/or inventory)

Liquid Asset.

Asset that can be turned into cash quickly,

within one year

Long-Term Liabilities.

Expenses, loans, and payables

due after one year

Net Profit.

Money left after all expenses have been paid.

Used to pay loan principal and to grow the company.

Net Sales.

Revenue or income from sales after returns

and allowances are deducted.

Net Worth.

Assets less liabilities. Show equity value.

Non-Current Assets.

Assets that take one year or more

to turn into cash.

Operating Lease.

Leases which allow you to buy the item

at the end of the lease, for a set price. These leases do not

appear on the Balance Sheet.

Owners’ Investment.

The money owners have invested

in a business.

Prime Rate.

The rate of interest lenders give to its prime

customers from time to time. Most business owners are

charged the prime rate plus a percentage.

Pro Forma.

Projecting or forecasting future income,

expenses, and cash flow.

Retained Earnings.

Net profits accumulated through

the company’s life and reported in the net worth or

equity section of the balance sheet. Note: Can be

negative if losses occur.

Secured Loan.

Loan secured by collateral (which will

be liquidated if the borrower defaults on the loan).

Tangible Asset.

Real property (machinery, equipment,

furniture and fixtures).

Term.

A loan’s maturity, stated in months or years.

Term Loan.

Loan, usually given in one lump sum at

the closing. Repayment is monthly over a stated term.

Trend Analysis.

Analysis of financial statements and

ratios to determine the financial strength over time.

Working Capital.

Difference between current assets and

current liabilities. An indication of liquidity and the ability

to meet current obligations.

GG ll oo ss ss aa rr yy

Printed by the Authority of the State of Illinois. W.O. 12-021 100 9/11 IOCI 12-261

www.ilsbdc.biz

The Illinois SBDC is funded in part through a

cooperative agreement with the U.S. Small Business

Administration and the Illinois Department of

Commerce and Economic Opportunity.

Mc Henry

Lake

De Kalb

Kane

Cook

Du Page

Kendall

Grundy

Will

Kankakee

Northeast Region

"Chicagoland"

Business Center Locations

SBDC

SBDC/ITC

SBDC/ITC/PTAC

SBDC/PTAC

PTAC

Technology Services